How the Crown Conquered the Conquests of the Conquistador

Why blueprints of imperial wealth extraction offer the modern allocator a historically tested asymmetrical refuge from structural fiat debasement.

Financial history is not merely a chronicle of dates, battles, and sovereign defaults; it is a meticulously documented laboratory of human behavior.

When observing the present macroeconomic landscape—characterized by soaring sovereign debt burdens, intractable structural inflation, and a profound geopolitical realignment—the tendency of the modern market participant is to treat these phenomena as utterly unprecedented.

They are emphatically not.

This is why we do Applied History.

Applied History

A practical tool that uses the laboratory of the past to better understand and navigate the complexities of the present and future.

Financial historians have observed a specific fiscal point that serves as the death knell for imperial hegemony: the moment when a nation’s interest payments on its national debt equal or exceed its expenditures on national defense.

Spanish Empire

The Spanish Empire:

Causes of Decline

Over-reliance on Debt Financing: Spain relied on a complex and expensive system of debt to finance its expansive military goals.

Fiscal Structural Issues: The tax system was highly regressive, relying on the lower classes while the nobility and clergy were largely exempt. The system was also fragmented by regional exemptions (fueros).

Inflationary Pressures: The influx of American silver caused a “Price Revolution,” which increased price levels and undermined the purchasing power of state revenues.

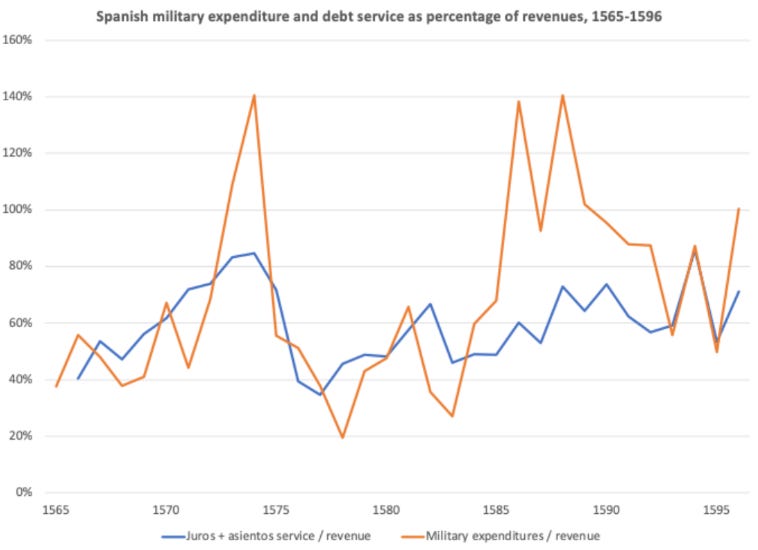

Rising Debt Service Costs: By the late 16th century, interest payments on long-term bonds (juros) consumed over 40% of annual revenues. By 1687, these payments absorbed 87% of Castilian revenues.

Punitive Borrowing Terms: Serial defaults forced the crown to borrow at increasingly high interest rates, sometimes reaching effective rates of 20%.

Vast Strategic Commitments: The empire faced immense costs to maintain forward-deployed infantry (tercios), secure global trade routes, and fight prolonged wars against the Dutch, the Ottomans, and the French.

Outcomes

Serial Defaults: Between 1557 and 1662, the Spanish crown defaulted on its debt eight times.

Erosion of Military Readiness: Mounting debt service obligations dwindled the resources available for the military, leading to endemic payment delays and supply shortages.

Loss of Military Predominance: Spain’s famed tercios were eventually surpassed by innovative military tactics from rivals, and its naval advantage was eclipsed by the English and Dutch.

Geopolitical Retreat: Fiscal constraints led to the formal recognition of Dutch independence in 1648, the independence of Portugal in 1640, and the ceding of territory to France in 1659.

Economic Contraction: The “Golden Age” of growth in the 16th century was followed by a contraction in the 17th century, partly due to investor lack of confidence and currency debasement.

British Empire

The British Empire:

Causes of Decline

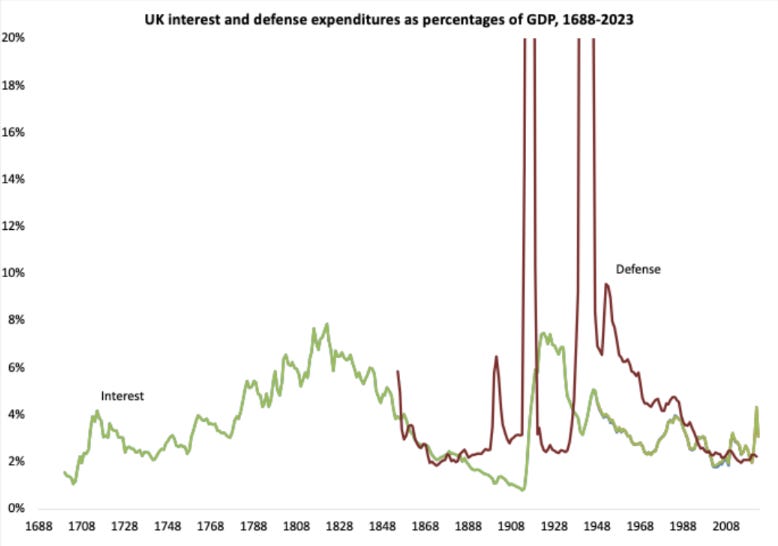

Wartime Debt Accumulation: Fighting the French Revolutionary and Napoleonic Wars drove the national debt from under 100% of GDP to a peak of 173% by 1822. Similarly, World War I increased the national debt by a factor of twelve, reaching 172% of GDP by 1927.

Rising Debt Service Costs: In the early 19th century, debt service consumed more than half of gross central government expenditure. In the interwar period (1920–1937), interest payments consistently exceeded military spending, peaking at 7.5% of GDP in 1923.

Post-War Economic Pressures: Following World War I, the economy contracted due to fiscal and monetary tightening while interest payments climbed.

The “Ferguson Limit”: Britain crossed the Ferguson limit (where interest payments exceed defense spending) during three distinct periods: 1857–1861, 1869–1884, and most notably 1920–1937. It crossed again in 2010 following the global financial crisis and subsequent shocks.

Outcomes

Strategic and Military Retrenchment: To return within fiscal limits in the 1920s and 30s, Britain adopted the “Ten-Year Rule” (a spending freeze for armed services) and reined in defense expenditure.

Hard Power Contraction: Fiscal constraints led to a reduction in troop numbers and the near-extinction of the Royal Air Force by the mid-1920s. In 1931, pay cuts led to the Invergordon Mutiny, which forced Britain off the gold standard.

Geopolitical Concessions and Appeasement: Britain participated in international arms-control agreements (like the Washington Naval Treaty) to avoid unaffordable arms races. The policy of appeasement in the 1930s was partly driven by the fear that higher armament spending would jeopardize economic recovery.

Transfer of Global Primacy: The Washington Naval Treaty marked the effective transfer of military primacy in the Western Hemisphere to the United States.

Decolonization and Financial Repression: After World War II, Britain jettisoned costly colonial commitments (e.g., India, Middle East) to manage its finances. It also used “financial repression” to inflate away the real value of war debt and interest payments.

Gradual Decline to “Militarily Inconsequential”: While Britain remained a great power through most of the 20th century, the sustained breach of the Ferguson limit starting in 2010 led to a state where it eventually became militarily inconsequential.

Ottoman Empire

The Ottoman Empire:

Causes of Decline

Fiscal Dependency and Foreign Debt: To modernize its infrastructure and military in the 19th century, the Ottoman government became increasingly dependent on high-interest foreign loans from British and French creditors.

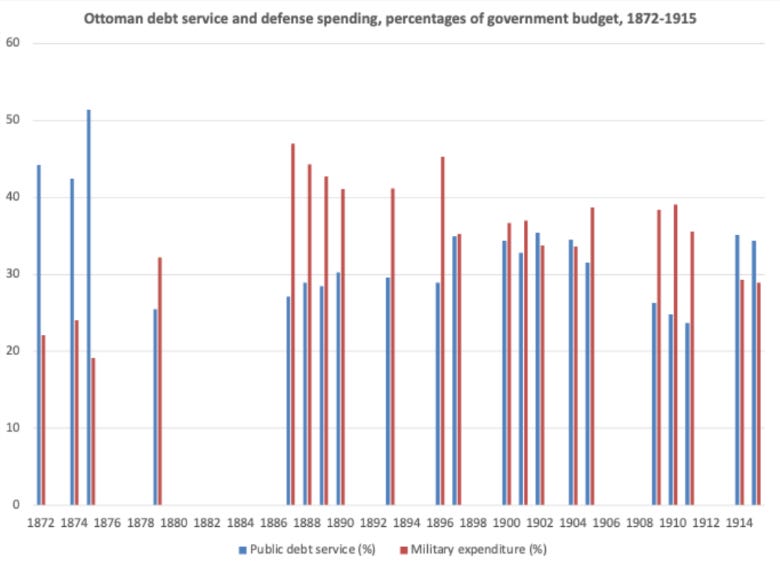

The “Ferguson Limit”: By the 1870s, interest payments on foreign debt consumed more than half of government revenues, far outpacing military expenditures. The empire crossed this limit several times between 1872 and 1915; in 1875, debt service exceeded military spending by a factor of 2.7.

Inability to Modernize: Legacy revenue methods were insufficient for the costs of modern statehood. Chronic underfunding left the empire unable to keep pace with rapid technological changes in European artillery, logistics, and training.

Economic Erosion: As global trade patterns shifted from Eurasia to the Atlantic, the empire’s economic base—formerly dependent on trade route customs and tariffs—eroded.

Outcomes

1875 Default: The empire’s fiscal crisis culminated in a formal debt default in 1875.

Diminished Sovereignty: In 1881, the Ottoman Public Debt Administration (OPDA) was established, placing European creditors in charge of vital revenue streams like tobacco taxes and customs duties. This reduced the empire to the “poor periphery” of the global economy.

Military Decay and Mutinies: Pay for officers and men frequently fell months into arrears, leading to 17 army mutinies by 1908.

Territorial and Diplomatic Loss: Underfunded forces suffered humiliating defeats in the Balkan Wars (1912–1913), resulting in the loss of productive lands. Weakness also undermined diplomatic credibility, as allies doubted the Porte’s capacity to fulfill commitments.

Vicious Cycle of Underinvestment: The fiscal rigidity imposed by foreign creditors created a cycle of underinvestment in heavy industry and transportation, further weakening the empire’s strategic position.

Austro–Hungarian Empire

The Austro–Hungarian Empire:

Causes of Decline

Fiscal Fragmentation: The constitutional Ausgleich of 1867 created separate parliaments and tax bases for the Austrian and Hungarian halves of the empire, leading to a dysfunctional “confederal” budget that relied on custom revenues and unpredictable annual appropriations.

Chronic Deficits: These institutional arrangements resulted in persistent budget deficits and a mounting public debt.

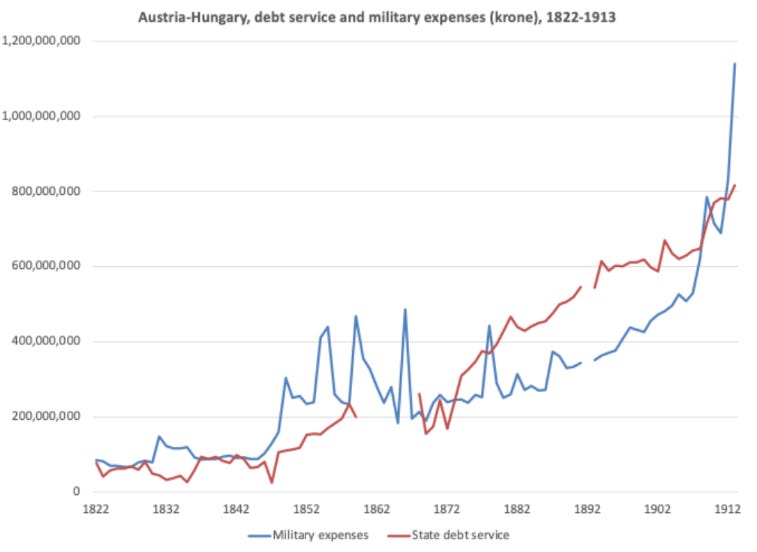

Prioritization of Debt over Defense: The empire consistently violated “Ferguson’s Limit” by spending more on debt servicing than on military modernization.

The Ferguson Limit: With the exception of a few brief years (1869–1873, 1878, 1909, and 1913), the Dual Monarchy remained in excess of the Ferguson limit for its entire existence. By the start of World War I, debt service consumed nearly 20% of the imperial budget, while defense spending lagged at just over 15%.

Internal Nationalism: Fiscal constraints limited resources, forcing the empire to prioritize certain regions, which exacerbated ethnic resentment and nationalist tensions, particularly in Hungary.

Outcomes

Military Under-Equipping: The empire struggled to provide its forces with sufficient modern rifles and artillery before and during World War I.

Failure of Deterrence: Fiscal and military weakness left Vienna unable to deter regional rivals, such as Belgrade, from pursuing reckless policies.

Naval Decline: The Imperial and Royal Navy could not maintain pace with regional rivals during the pre-war dreadnought arms race.

Strategic Weakness: The empire became known as the “second weakest among the great powers,” spending just enough on the army to ensure it remained vulnerable.

Revolution and Dissolution: Like other empires that succumbed to fiscal crisis, the Austro-Hungarian Empire eventually faced imperial dissolution following the protracted conflict of World War I.

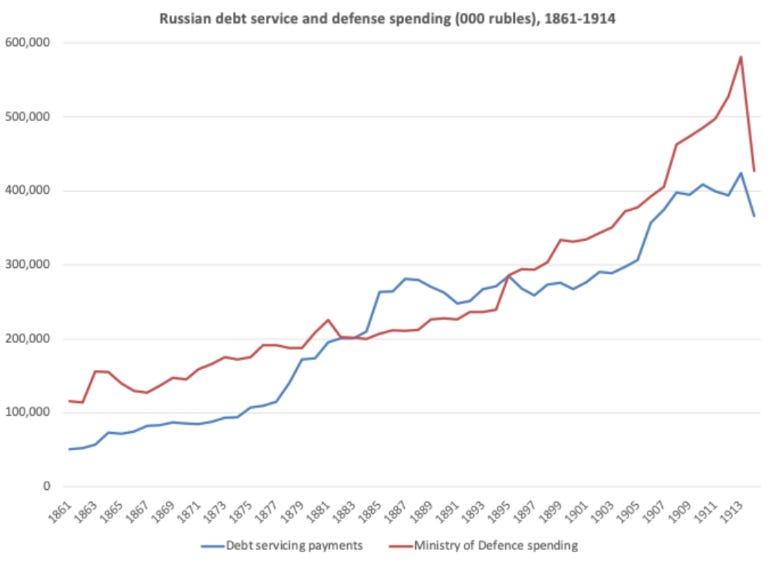

Russian Empire

The Russian Empire:

Causes of Decline

Chronic Deficits: In the mid-19th century, Russian finances were characterized by “chronic deficit”.

Rising Borrowing Costs: In the decade leading up to 1885, the empire’s cost of borrowing doubled.

Wartime Fiscal Strain: Protracted global conflict eventually became unsustainable, leading to fiscal crises that culminated in revolution.

Peacetime Arms Race: The fiscal strains of the peacetime arms race prior to World War I became domestically intolerable, which may have tempted the empire to risk war.

Outcomes

Fiscal Stabilization: Under Finance Minister Count Sergei Yulyevich Witte (1892–1903), the Tsarist system was stabilized by bringing it back into compliance with Ferguson’s Law, ensuring defense spending outpaced debt service.

Military Readiness: On the eve of World War I, the Russian Empire was on a sound fiscal footing, with defense spending significantly higher than debt servicing.

Imperial Dissolution: Despite being compliant with Ferguson’s Law before 1914, the empire could not survive the fiscal crisis brought on by a protracted global conflict, resulting in revolution and debt default.

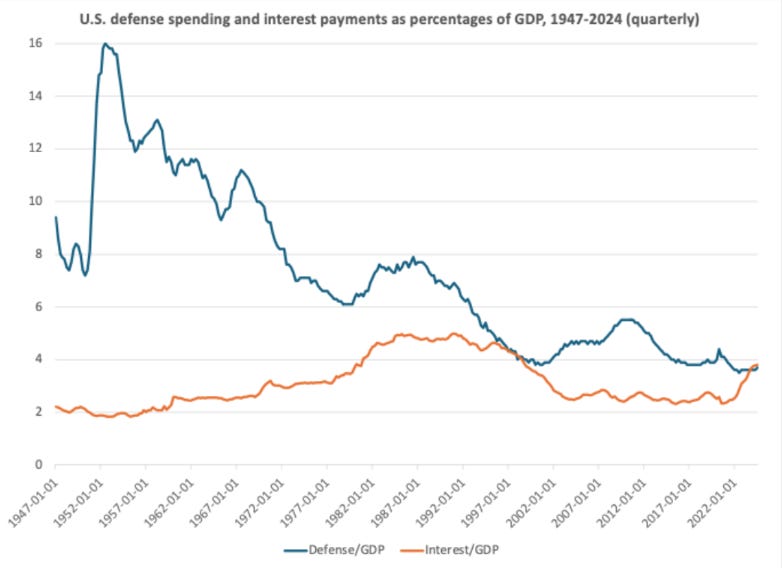

The United States

The United States:

Current Challenges

Surpassing the “Ferguson Limit”: In 2024, U.S. net interest outlays reached 3.1% of GDP, exceeding defense spending (3.0%) for the first time in nearly a century.

Rising Debt Burden: Federal debt is projected to exceed 120% of GDP this year, a level higher than the peak following World War II.

Sensitivity to Interest Rates: Unlike historical Britain, which held much of its debt in long-term annuities, modern U.S. debt has a short average maturity (69 to 73 months), making it highly sensitive to rising interest rates.

Mandatory Spending Pressures: Entitlement programs like Social Security and Medicare are the largest federal expenditures and are becoming more expensive due to an aging population and unfavorable demographics.

Unplanned Fiscal Shifts: As recently as 2020, the government projected interest payments would not exceed defense spending until 2028; however, this “tipping point” arrived years early.

Outcomes and Projected Future Impacts

Sustained Violation of Ferguson’s Law: Current projections indicate a continued breach of the Ferguson limit, with net interest payments potentially doubling the defense budget by 2049.

Erosion of Hard Power: Rising debt service costs create a “vicious circle” that pulls scarce resources away from national security, research, and advanced military technologies.

Vulnerability to Rivals: History suggests that remaining above the Ferguson limit for an extended period signals geopolitical weakness and emboldens rivals to challenge the great power’s global leadership.

Failure of Deterrence: Reduced defense outlays undermine the credibility of a great power’s deterrent, potentially increasing the payoffs for aggression by revisionist states.

Need for a “Productivity Miracle”: Without radical reforms to entitlement programs, the only plausible way for the U.S. to return within the Ferguson limit may be through a massive productivity boost, such as one driven by artificial intelligence.

Throughout history, from the waning days of the Spanish Empire to the twilight of the French monarchy to the modern day United States, this specific fiscal limit has signaled a transition from dominance to decline.

In the modern context of the United States, as interest payments consume an increasingly vast percentage of gross domestic product, the options available to the sovereign narrow dramatically.

In such environments, the only politically palatable exit from crushing debt burdens is the deliberate, systematic debasement of the currency.

Inflation, therefore, is not a transitory anomaly resulting from post-pandemic supply chain disruptions; it is a structural, mathematical necessity for the preservation of the indebted state.

Looking back at the past and then at the present, one might conclude something akin to King Théoden.

Nonetheless, we should not forget that:

Faced with the inevitable erosion of fiat purchasing power, the conventional reflex of the capital allocator is to seek refuge in hard assets.

John Maynard Keynes famously dismissed the gold standard as a “barbarous relic”.

Yet, when geopolitics render fiat reserves weaponizable and inherently untrustworthy—as witnessed in the aftermath of the Russian invasion of Ukraine and the subsequent freezing of Russia’s central bank assets—capital inevitably returns to this ancient anchor.

However, the mere accumulation of physical gold bullion is a static defense.

It offers preservation, but not necessarily real wealth creation.

Here we will discuss why the traditional choice of precious metal miners are fundamentally flawed as a vehicle for inflation protection, and why the royalty/streaming business model represents the more asymmetric, capital-light compounding choice especially in light of financial history.

By learning from the historical precedents of the quinto real and tax farming, we will demonstrate why precious metal royalty/streaming companies are asymmetric, capital-light, compounding choices especially in light of lessons learned from applied financial history.

The Quinto Real and Tax Farming

To grasp the profound economic superiority of the precious metal royalty/streaming business model, it is necessary to examine how empires historically maximized wealth extraction without bearing the operational risks of conquest, logistics, and administration.

The blueprints for modern precious metal financing were drawn centuries ago, forged in the mountains of the New World and refined in the administrative corridors of early modern Europe.

The fundamental challenge of resource extraction has always been the immense capital requirement and the inherent operational danger.

The solutions devised by historical sovereigns mirror the financial mechanisms utilized by today’s leading royalty/streaming companies.

The Caustic Conquests of the Conquistador

In the sixteenth century, the Spanish Empire stumbled upon the greatest concentration of precious metals in human history, most notably at Cerro Rico in Potosí, Peru.

Between the years 1500 and 1800, these mines produced an astounding 150,000 tons of silver and 2,800 tons of gold, amounts that fundamentally altered global trade dynamics and triggered the prolonged inflationary period in Europe known as the Price Revolution.

Yes, a massive new supply of gold and silver caused inflation.

This is what happens when you have a high stock-to-flow ratio i.e. a lot of new supply relative to the size of existing supply.

We cover this variable in the context of what is money here:

The operational realities of this extraction were brutal for those doing the actual physical work.

Still, the popular historical imagination often pictures the conquistadors returning to Europe drowning in boundless wealth.

As we say ad nauseam:

A partial truth is more dangerous than a lie.

The financial reality was far grimmer.

The conquistadors were entirely responsible for funding their own expeditions, purchasing equipment, securing labor, and establishing supply lines.

They bore the totality of the capital expenditures and operating expenses.

Despite extracting unimaginable physical wealth from the earth, many conquistadors died heavily indebted, their profit margins utterly crushed by the logistical nightmares and exorbitant costs of their operations.

The Spanish Crown, conversely, engaged in a far more lucrative financial arrangement.

The Crown retained the ultimate rights to the land and demanded a fixed percentage of all treasure extracted—a 20 percent top-line tribute known as the quinto real, or the royal fifth.

In the later Spanish expansions into the Americas, the Crown did not finance the ships crossing the Atlantic, it did not provision the miners, and it did not operate the smelters.

It simply collected a royalty on the gross production of the enterprise.

The quinto real was a mechanism of pure, frictionless leverage.

The Crown captured the upside of new geological discoveries and rising metal flows while entirely insulating itself from cost overruns, operational failures, inflation of input costs, and capital destruction.

If a mining expedition failed due to disease or logistical collapse, the Crown lost nothing, having invested nothing.

If the expedition succeeded, the Crown collected its top-line revenue.

This absolute separation of upside participation from downside operational risk is the theoretical foundation of the modern royalty/streaming company.

Tax Farming: Privatizing the Imperial Toll Road

A parallel evolutionary step in the development of the streaming model was the practice of “tax farming,” utilized extensively in early modern France, Britain, and the Ottoman Empire.

Rather than building a sprawling, expensive, and often corrupt state bureaucracy to assess and collect levies, sovereign powers would auction the right to collect taxes to private financiers or syndicates, such as the Ferme Générale in France.

The mechanics of tax farming were remarkably similar to modern streaming agreements. The financiers would pay the state an upfront lump sum—providing immediate, non-dilutive capital to the sovereign, which was frequently utilized to fund wars or alleviate immediate debt burdens.

In exchange for this upfront capital provision, the financier acquired the right to collect and keep the future tax revenues from a specific region, trade route, or commodity monopoly for a set number of years.

While tax farming eventually fell out of favor due to the political optics of private wealth extraction and the eventual centralization of the nation-state, its underlying financial architecture was most appealing to the perspective of the investor.

It converted an unpredictable, future revenue stream into immediate capital for the operator (the state), while the financier acquired a long-duration asset with embedded optionality and minimal ongoing operational costs. The tax farmer did not produce the goods being taxed; they simply sat atop the economic chokepoint and collected a margin.

Modern precious metal royalty/streaming companies are the descendants of the quinto real and the tax farmer.

They represent a financial model that strips the toxic, capital-intensive elements away from resource extraction, leaving only a pure, high-margin, capital-light revenue stream that compounds relentlessly over time.

A revenue stream which flows from the headwaters of the debasement resistant monetary medium that is gold.

The “Barbarous Relic” Strikes Back

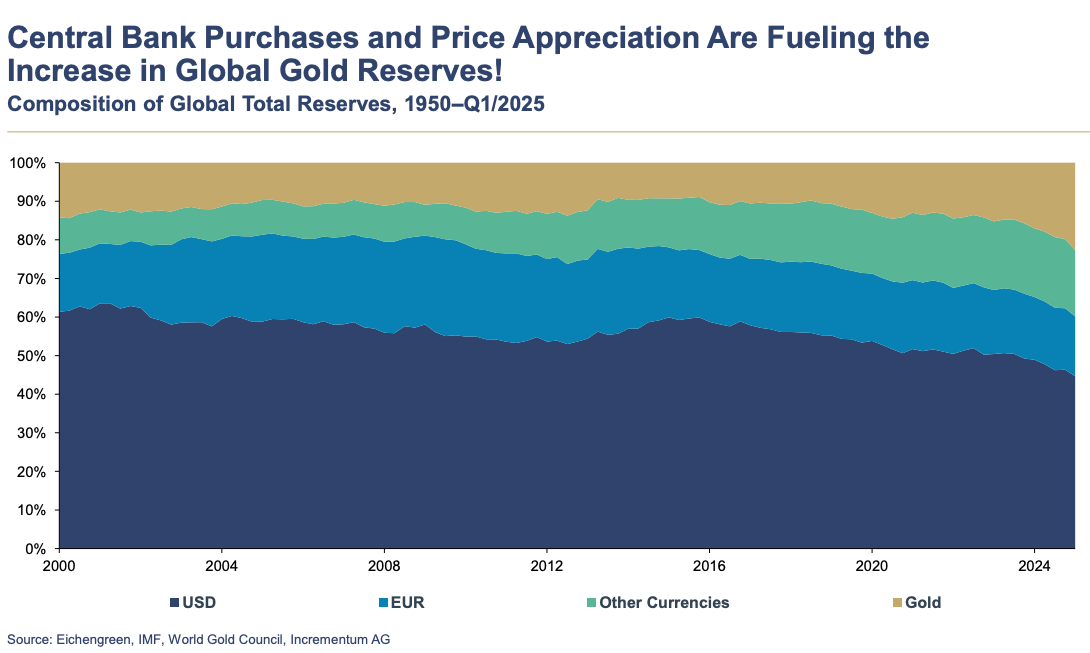

To fully appreciate why these modern capital-light extraction models that sit atop the debasement resistant monetary medium that is gold are especially important in contemporary portfolio construction, one must understand the macroeconomic forces driving gold’s rediscovery.

The global monetary system is currently undergoing a profound phase transition, driven by the weaponization of finance and the inescapable mathematics of sovereign debt.

The Weaponization of Fiat Reserves

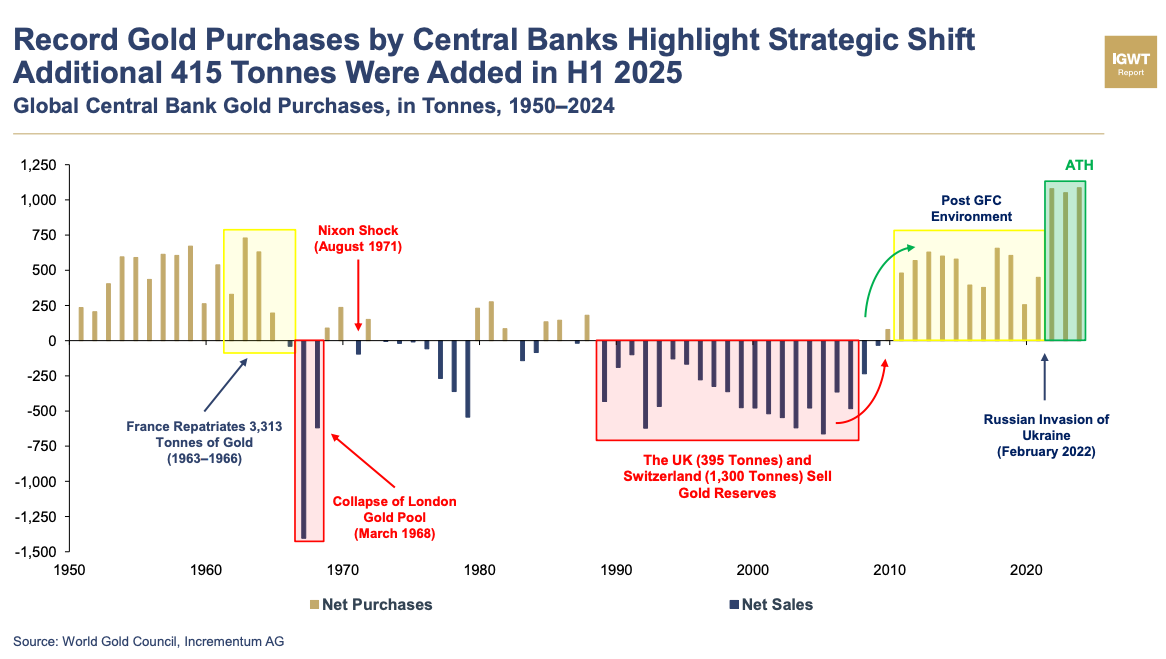

For decades following the collapse of the Bretton Woods system in 1971, the prevailing economic orthodoxy held that fiat currencies, managed by independent central banks, had rendered physical precious metals obsolete.

Keynes’s derisive classification of the gold standard as a “barbarous relic” became the accepted wisdom of the financial establishment. Gold produced no yield, incurred storage costs, and was viewed as an anachronism in an era of digital, frictionless capital flows.

However, the geopolitical events of recent years have shattered this illusion.

The decision by Western powers to freeze the foreign exchange reserves of the Russian central bank as punishment for Russia’s invasion of Ukraine served as a stark realization for sovereign states globally.

Fiat reserves held in foreign jurisdictions are not risk-free assets; they are uncollateralized liabilities subject to immediate confiscation by the issuer.

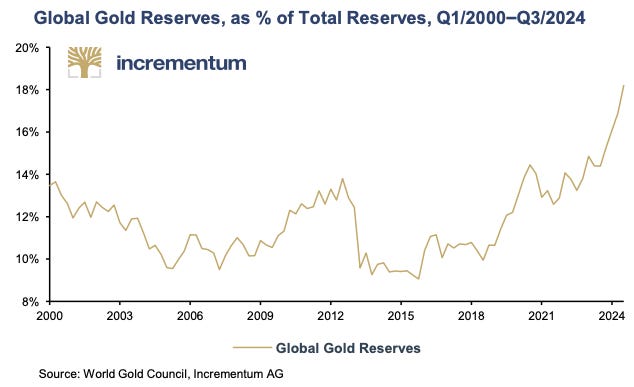

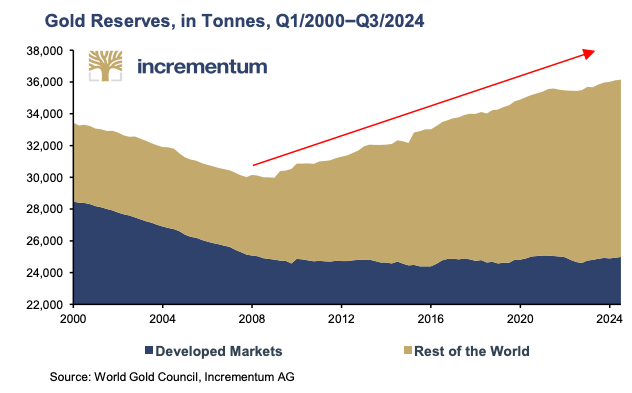

Consequently, global central banks have accelerated their demand for physical gold at an unprecedented pace, specifically opting for physical repatriation and delivery to highlight a growing mistrust in ledger-based fiat systems.

As we were writing this, France pulled the last of its gold from New York, marking the first time since the late 1920s that France has stored no gold with the US.

Reuters reports on the matter stated that “politics were not involved”.

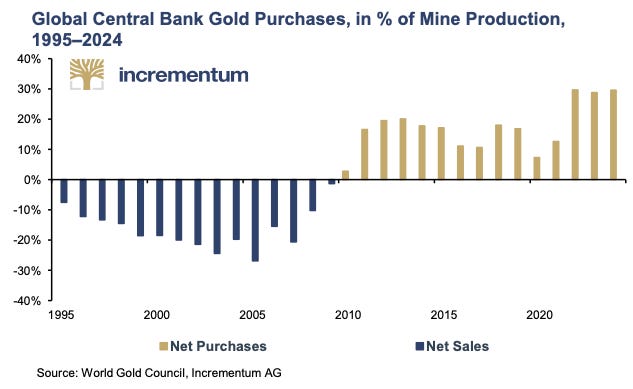

Furthermore, the structural depreciation of fiat currency is accelerating.

While central bankers frequently cite low single-digit inflation targets, a broader historical analysis reveals a more severe debasement.

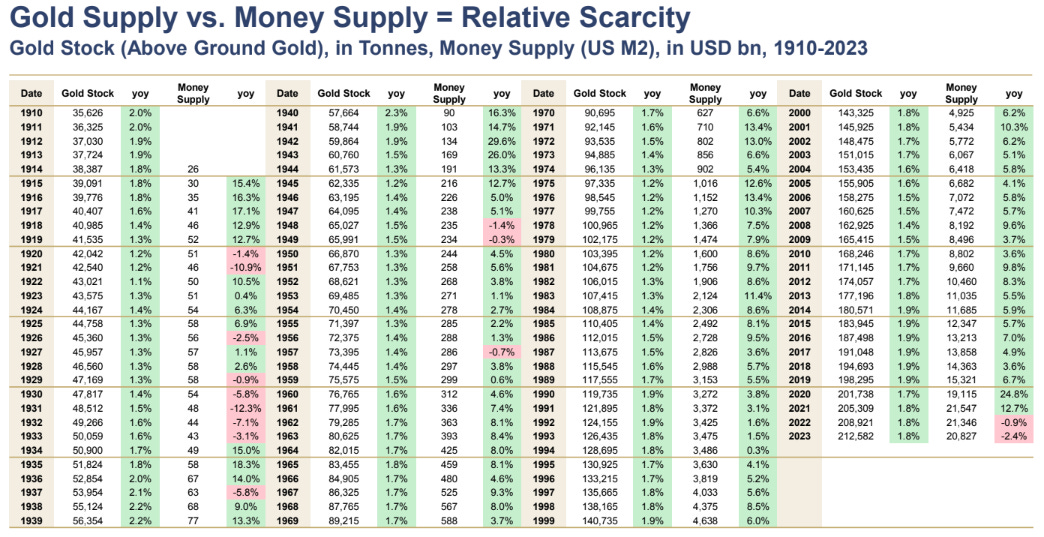

Over the past century, the global supply of gold has increased at an annualized rate of approximately 1.59%, constrained by the geological difficulty of extraction.

Conversely, the supply of the United States dollar has increased at an annualized rate of over 8.6% during the same period. The true, real rate of fiat debasement is significantly higher than official consumer price indices suggest, rendering the pursuit of hard assets not merely a speculative endeavor, but a mathematical necessity for the preservation of purchasing power.

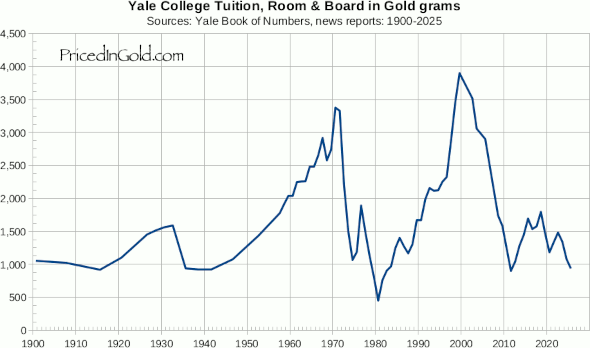

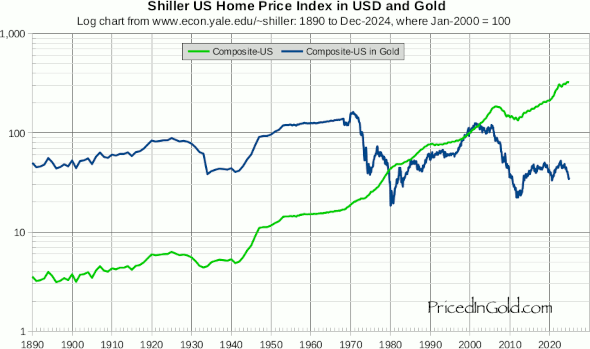

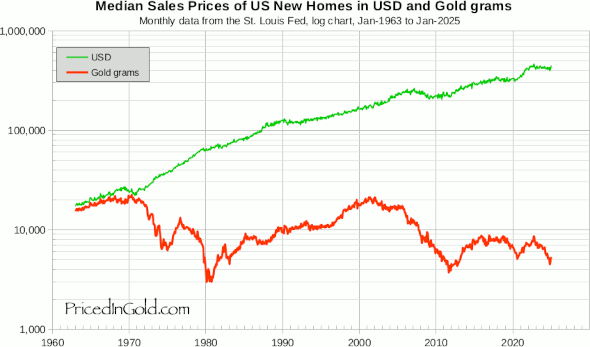

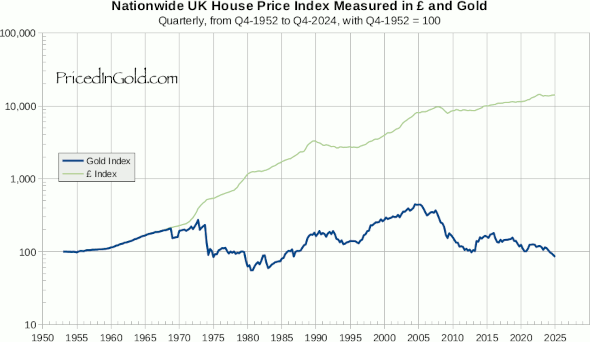

It’s a monetary illusion to say goods/services like housing or college tuition are getting more expensive (the numerator).

In reality, goods/services only seem more expensive because fiat currency is losing its purchasing power (the denominator).

The Structural Flaws of Traditional Mining

The prevailing assumption among generalist capital allocators is that investing in a gold or silver mining company provides leveraged, equity-based exposure to the price of the underlying metal.

If the price of gold rises by 10%, the operating leverage of the miner should theoretically cause its equity valuation to rise by 20% or 30%.

The historical record, however, exposes this assumption as a perilous fallacy.

The traditional mining business is plagued by a structural paradox that routinely destroys shareholder value during the exact macroeconomic environments where it is expected to outperform.

The Cruel Paradox of Gold Miners in Inflationary Environments

During periods of material monetary expansion and fiat debasement, the nominal price of precious metals naturally rises.

In the immediate, short-term aftermath of a price spike, a miner’s revenues will increase, driving a sudden surge in profitability because the costs associated with pulling that specific ounce out of the ground were incurred in the past.

However, this profitability is fleeting.

Driven by the prospect of higher margins and pressured by shareholders to demonstrate growth, mining management teams inevitably seek to expand existing operations or acquire new, lower-grade deposits that were previously deemed uneconomical.

This expansion requires vast amounts of physical capital and industrial inputs.

New acreage must be secured, massive earthmoving equipment must be purchased, replacement parts must be stockpiled, and specialized labor must be hired.

In an inflationary macroeconomic environment, the competition for these finite resources triggers a severe, cascading spike in input costs.

The cost of diesel fuel, steel, cyanide for leaching, electricity, and human capital all surge simultaneously.

Therefore, the very macroeconomic forces that drive the price of gold higher generally drive the cost of extraction higher, and historically, input costs inflate at a faster rate than the end commodity.

The mining industry is thus structurally trapped in a classic boom-and-bust cycle.

By the time the new, highly capitalized mine expansions finally come online and surge new supply into the market, the commodity cycle has often peaked. The gold price retreats precisely as the miner’s cost structure hits its zenith, resulting in catastrophic margin compression, impaired assets, and massive value destruction for equity holders.

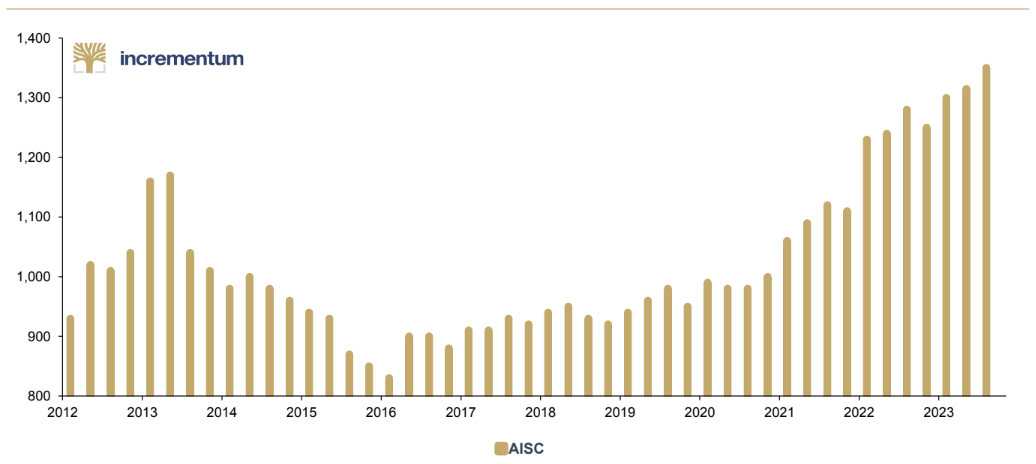

In the chart below, you can see what the All-in Sustaining Cost (AISC) of extracting 1 ounce of gold in USD and how it has increased over time.

The Burden of Capital and Operational Risk

Beyond the inescapable inflation paradox, traditional miners face a gauntlet of existential threats that cannot be accurately modeled on a discounted cash flow spreadsheet. The extraction of precious metals from the earth’s crust is an exercise in immense operational hazard.

Miners must navigate intense geopolitical risks, as their assets are immobile and frequently located in resource-rich but economically unstable jurisdictions.

Governments facing their own debt crises frequently alter tax regimes retroactively, demand larger equity stakes in domestic projects, or outright nationalize mining assets.

Furthermore, miners are burdened with unpredictable exploration expenses, volatile labor relations, and immense post-production liabilities, such as mine reclamation and environmental remediation. A single environmental disaster or a prolonged labor strike can bankrupt a highly leveraged mining operation entirely.

These compounding vulnerabilities explain why the broader equity market has largely abandoned the sector.

Despite the critical nature of the commodities they produce, the entire mining segment of the S&P 500 Index represents a trivial 0.2% weight, consisting of merely one copper miner and one gold miner.

The traditional mining model is an exercise in Sisyphean capital destruction: billions of dollars must be continually pushed back into the earth simply to maintain flat production profiles, leaving paltry amounts of free cash flow to be distributed to shareholders.

The modern miners are the conquistadors of the 21st century, bearing the totality of the capital expenditures, suffering the brunt of cost inflation, and absorbing all operational risks, while the margins are squeezed relentlessly from all sides.

The Modern Royalty/Streaming Model

If traditional mining is the grueling, capital-destructive work of the conquistador, the royalty/streaming business is the modern, highly refined manifestation of the crown.

It is a financial innovation that elegantly and completely separates commodity price exposure from operational cost inflation.

The Mechanics of the Financing Model

The royalty/streaming business model operates entirely on a principle of capital provision and contractual rights.

A royalty/streaming company does not operate mines, it does not hire geologists or truck drivers, and it does not purchase earthmovers. Instead, it functions as a highly specialized financier, providing liquidity to an industry that is generally starved for capital.

When a traditional mining company requires hundreds of millions, or even billions, of dollars to construct a new mine or expand an existing operation, it faces a severe financing dilemma.

Traditional debt financing from commercial banks is highly risky; a temporary drop in commodity prices or a delay in construction before the mine is fully operational can lead to immediate insolvency.

Conversely, equity financing via the public markets is often highly dilutive to existing shareholders, permanently impairing their per-share value.

The royalty/streaming company steps into this void to provide the required upfront capital. In exchange for this non-dilutive, non-recourse funding, the financier receives one of two distinct contractual rights :

A Royalty (e.g., Net Smelter Return - NSR): The right to receive a fixed percentage of the gross revenue generated from the mine’s future production. The NSR is calculated net of minor downstream costs such as transportation, refining, and smelting, but crucially, it is calculated before any of the mine’s operating costs or capital expenditures are deducted.

A Stream: The right to purchase a fixed percentage of the mine’s future physical metal production at a predetermined, deeply discounted price.

The mathematical discount inherent in a streaming contract is often staggering to those unfamiliar with the sector.

A typical streaming contract might grant the financier the right to purchase future gold production for $400 per ounce, or silver for $4 per ounce, while the spot market prices trade at multiples of those figures.

This deep discount is not a market anomaly or an exploitative practice; it is simply the present value of the massive upfront capital provided to the miner, amortized over a 20-to-30-year mine life, incorporating a required double-digit rate of return (typically in the 12% to 15% range). The streaming company earns that discount over time through the power of compounding.

Fixed Costs and Free Optionality

The defining brilliance of this financial architecture is its total insulation from operational expenditures and cost inflation. If the global price of diesel fuel doubles, if the cost of steel skyrockets, or if the mine’s unionized workforce strikes for a 20% wage increase, the traditional mining operator absorbs the entirety of the financial blow. The streaming company, however, continues to pay its contractually fixed delivery price of $400 per ounce.

Thus, as the spot price of gold or silver rises in an inflationary regime, the royalty/streaming company’s profit margins expand dramatically and immediately, making it the ultimate beneficiary of monetary debasement. Unlike the miner, whose margins could compress due to rising input costs, the royalty/streaming company’s costs are contractually frozen.

Furthermore, royalty/streaming companies acquire what can best be described as “free, asymmetric optionality.”

Royalty/streaming contracts are typically tied to vast geographical land packages rather than just the initial, delineated mine footprint.

Over the decades-long lifespan of a mine, the operating company will continually use its own capital to conduct further exploration drilling. If the operator discovers a massive new deposit on the property, the royalty/streaming company’s claim automatically extends to the new discovery. The royalty/streaming firm gains years, or even decades, of extended cash flow without having to invest a single additional dollar in exploration, drilling, or development.

Conclusion: An Allocation of Applied History

As the timeline advances through the latter half of the 2020s, the global macroeconomic architecture bears a striking resemblance to the most volatile periods of the 1970s and the early 20th century.

The post-Cold War globalization dividend—which provided three decades of relentless, disinflationary labor arbitrage by bringing three billion workers into the global market—has permanently fractured.

In its place, a multipolar world has emerged, characterized by the frantic onshoring of supply chains, the weaponization of central bank reserves, and an explosive, energy-intensive technological arms race in artificial intelligence.

Simultaneously, the sovereign debt profiles of many nations have crossed the historical rubicon where mandatory interest expenses rival the funding required to maintain geopolitical deterrence.

History is unsentimental regarding the resolution of such crises: sovereign states do not voluntarily default on their nominal obligations; they default in real terms through the deliberate, sustained inflation of the currency supply.

Allocators should consider assets that exhibit true asymmetric optionality: businesses that capture the upside of rising commodity prices without absorbing the crushing, simultaneous inflation of operating expenditures and capital requirements.

Select precious metal royalty/streaming companies are not merely derivatives of the mining sector; they are the most highly refined expressions of capital-light economics ever engineered in the hard asset space.

Select Exposures

These are the characteristics of our precious metal royalty/streaming investments.

Exposure 1

Royalty and Streaming Financier: It provides upfront capital to mining companies in exchange for either a royalty (a percentage of the mine’s future revenue) or a stream (the right to buy future metal production at a fixed, low price). It is a financier, not a mine operator.

Holds a Vast, Diversified Portfolio: Its assets include hundreds of royalties and streams, primarily in gold, but also silver, platinum group metals, and other commodities. This diversification across different assets, geographies, and operators significantly reduces single-project risk.

Maintains Exposure to Oil & Gas Royalties: Uniquely among its peers, it also holds a significant portfolio of oil and gas royalties. This provides an additional layer of commodity diversification and a hedge against different economic cycles.

Gains “Free” Optionality on Exploration: A core part of its model is acquiring royalties on vast land packages. If the mining partner discovers more resources on that land, its royalty interest applies to the new discoveries without it having to invest another dollar in exploration or development costs.

Exposure 2

Pioneered the Precious Metals “Streaming” Model: It specializes in streaming agreements. They make a large, upfront payment to a mining company and in return receive the right to buy a percentage of that mine’s future gold or silver production at a deeply discounted, fixed price (e.g., ~$400/ounce for gold).

Targets By-Product Metals from Base Metal Mines: A key strategy is to provide capital to miners of base metals like copper or zinc. These miners often treat the gold and silver produced alongside their primary metal as a secondary “by-product.” It unlocks the value of these precious metals for the miner, securing the stream for themselves.

Secures Contracts on Large, Long-Life Assets: It focuses on partnering with major mining companies on large-scale, low-cost mining operations. This ensures their streams are tied to assets that will be producing metal for decades, providing highly predictable, long-term cash flow.

Creates Massive Margin Expansion: Because its purchase price is fixed by contract, its profit margin expands dramatically as the spot price of gold and silver rises. Unlike a miner, its costs do not inflate with the price of the commodity, a key feature for an inflation hedge.

Offers a “Pure-Play” Streaming Investment: It focuses exclusively on precious metals streaming, primarily gold and silver. This provides us with direct, high-leverage exposure to precious metals prices without the complexities of other commodities or royalty types.

What they have in common:

Buy Low ; Sell High: Royalty/Streaming companies provide upfront capital to mining companies in exchange for the right to receive a portion of future production (typically gold, silver, or other precious metals) at a fixed, discounted price or as a percentage of output.

Avoids Cost Overruns: Unlike traditional miners, royalty/streaming companies do not operate mines themselves; they earn revenue streams based on the exploration and production activities of third-party operators/miners.

Capital Light Businesses: These companies are considered "capital-light" because they avoid the significant capital expenditures, operating costs, and post-production liabilities associated with direct mining operations.

Positive Asymmetric Optionality: This structure offers "asymmetric optionality": revenues can increase both from higher metals prices and from increased production at the underlying mines, while the company itself bears minimal ongoing costs.

Inflation Protection: Precious metals generally perform well in inflationary environments, and these companies provide magnified exposure to these price movements, making them potentially inflation beneficiaries.

All-Weather Resilience: They can perform well in various economic regimes (high/low growth, high/low inflation), not just during inflationary periods.

Long-Duration Assets: Many agreements are tied to long-life mines, sometimes with decades or even centuries of production potential, providing enduring revenue streams.

Optionality and Scarcity Value: As new mine discoveries become rarer and existing high-quality assets more valuable, holding royalties/streams on these assets becomes increasingly advantageous.

Mine Diversification: Royalty/Streaming companies often hold interests in multiple mines and jurisdictions, reducing concentration risk and increasing the stability of cash flows.

Disclaimer

This website is not an offer or solicitation in any jurisdiction in which the firm is not registered. Information presented is for educational purposes only. It should not be considered specific investment advice, does not take into consideration your specific situation, and does not intend to make an offer or solicitation for the sale or purchase of any securities or investment strategies. The services, securities and financial instruments described on this website may not be suitable for you, and not all strategies are appropriate at all times. Investments involve risk and are not guaranteed. Past performance is not necessarily a guide to future performance. Independent advice should be sought in all cases.

TYME Advisors is a U.S. Securities and Exchange Commission (SEC) Registered Investment Advisor . Registration does not imply a certain level of skill or training. Information about the firm including the Customer Relationship Summary is available on the SEC’s website at www.adviserinfo.sec.gov. Information about our privacy policy is located here.