The Icarus Public Offering (IPO)

Strap On Your Wax Wings (or SpaceX's Falcon Wings) and soar into the Warmth of The Sun's Stellar High Valuations

If one surveys the grand, intoxicating tapestry of financial history—from the railway manias of Victorian England to the dot-com euphoria at the turn of the millennium—a singular, unyielding truth emerges: human beings possess an inexhaustible desire to “get in on the ground floor.”

There is an ancient Greek myth that perfectly captures the modern retail investor’s experience with the Initial Public Offering (IPO): the tragedy of Icarus.

Intoxicated by the thrill of flight, Icarus ignored all warnings and flew too close to the sun; his wax wings melted, and he plunged into the abyss.

Today, Wall Street routinely invites the public to strap on their own wax wings and chase the soaring valuations of newly minted public companies.

It appears to be a glorious engine of wealth creation. But if we peel back the gilded veneer, who is actually making the money, and who is destined to fall from the sky?

Where are the Customer’s Yachts?

Let us demystify the architecture of the IPO, examine the perverse incentives that drive it, and look at the looming, colossal test case: the unprecedented IPO of Elon Musk’s SpaceX.

The Architecture of an IPO

At its core, an IPO is simply the transition of a company from private ownership to public ownership. A private enterprise decides to offer shares of itself to the broader public, ostensibly to fund grand new growth initiatives or raise its public profile.

Yet, there is a second, far more potent motive: liquidity. Going public allows the company’s founders, corporate insiders, and early venture capitalists to finally cash out the private shares they have been holding for years.

To orchestrate this grand debut, the company hires a “lead underwriter”—a prestigious investment bank—which in turn forms a “syndicate” of other banks to distribute the shares to the public. For a handsome fee, these bankers gauge the mood of the market and guarantee an “offering price”.

Herein lies the trap. You must understand the divergent motivations of the players involved:

The Insiders

They wish to sell their shares at the highest conceivable valuation to maximize their newfound fortunes.

The Investment Bankers

Their imperative is to generate euphoric demand, successfully offload the shares, collect their underwriting fees, and minimize their own risk.

The Institutional “Whales”

These are the elite, high-net-worth clients and massive institutional funds who are granted exclusive access to buy the shares at the official IPO offering price.

The Retail Investor (You)

Because demand for a hot IPO invariably exceeds supply, everyday investors are functionally locked out of buying at the initial offering price. You are only permitted to buy the stock after it begins trading on the secondary market—which is to say, after the price has already been driven up by the whales.

The First-Day Pop

When the financial press breathlessly reports that an IPO “soared 20% on its first day,” they are referring to the difference between the exclusive IPO offering price and the “first closing price” at the end of the trading day.

Historically, this pop is a very real phenomenon; between 1980 and 2024, the average first-day return for an IPO was around 18.9%.

But here is the cruel irony: you did not earn that return. The institutional whales who were allocated shares at the offering price captured that gain. If you are an ordinary investor, you likely bought in at that inflated first closing price.

When we examine the long-term performance of these companies, the data is positively sobering. A comprehensive analysis of thousands of IPOs reveals that over their first three years, IPOs underperform the broader market by an average of 20.5%.

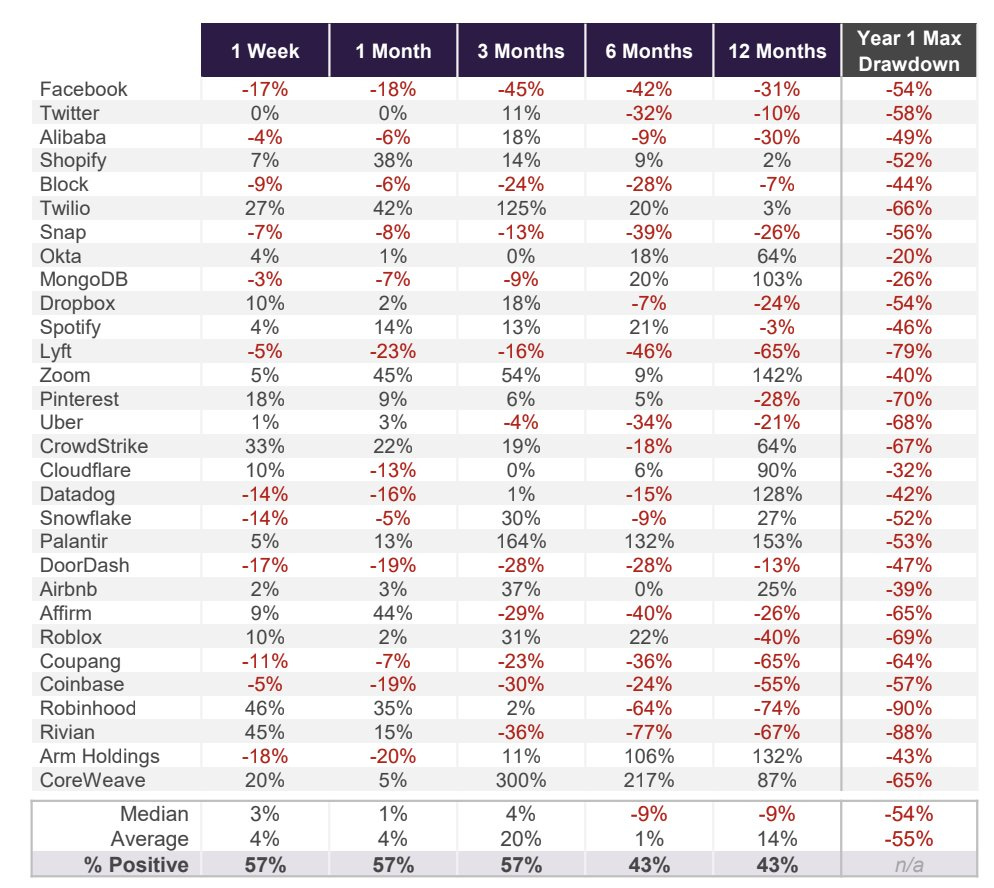

Here are some recent examples of IPOs as well.

Your financial destiny in an IPO is materially dictated by the side of the velvet rope on which you stand.

To compound this misery, the retail investor suffers from a brutal “selection bias”.

If you attempt to buy into every IPO, you will find your orders fully filled only on the overpriced disasters that the institutional elites actively avoided. For the truly underpriced, highly desirable companies, you will be allocated merely a fraction of what you requested.

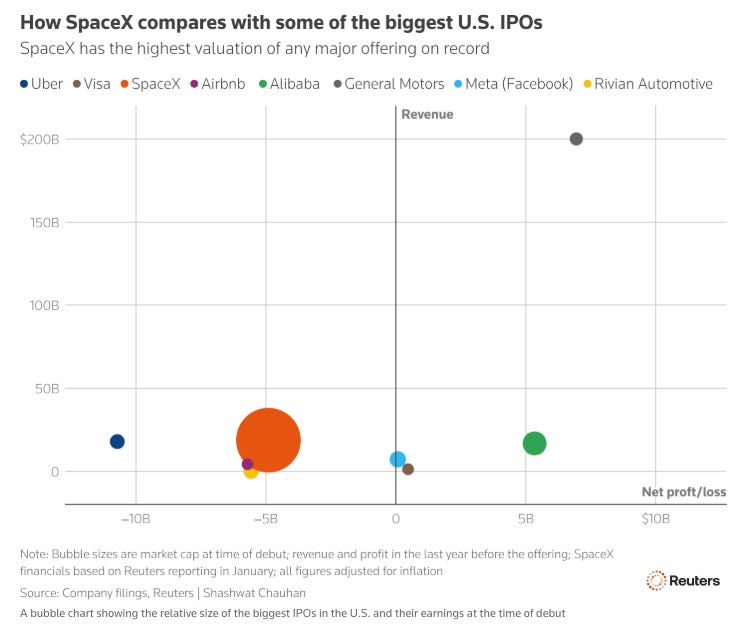

The Ultimate Spectacle: The SpaceX Mega-IPO

To observe these dynamics operating at a world-historical scale, we need look no further than the impending IPO of SpaceX.

It is a company of undeniable, world-beating technological prowess. Yet, at a proposed valuation of $1.75 trillion, it is poised to be the largest IPO in human history by a staggering margin.

Ok Icarus, let us quickly examine these Falcon 9 wings:

The Terrestrial Limits of Starlink

The astronomical valuation relies heavily on the continued hyper-growth of Starlink, its satellite internet business (it is also the customer for 78% of its Space launches).

But Starlink faces a terrestrial reality: 90% of US locations already possess gigabit internet access, and fiber-optic networks will reach 80% to 85% of homes by the end of the decade. Because satellite internet simply cannot compete with fiber on a per-bit pricing basis, Starlink’s domestic subscriber ceiling is functionally capped at roughly 15 million1.

It is a magnificent solution for remote areas, but it does not underwrite a near two-trillion-dollar empire.

After all, space is hard.

Iridium spent $5 billion and filed for bankruptcy in 1999. OneWeb raised $3.2 billion and collapsed in 20202.

Governance as a Fiefdom

When you purchase shares in SpaceX, you are not buying into a conventional public corporation; you are becoming a minority subject in Elon Musk’s personal fiefdom.

Musk controls 85.1% of the voting power, rendering outside shareholders utterly powerless.

Furthermore, the prospectus discloses over $20 billion in obligations to other Musk-affiliated entities, laying bare the profound risks of self-dealing3.

Opaque Accounting

Adding to the opacity, SpaceX recently absorbed Musk’s artificial intelligence venture, xAI, using a method known as “common control” accounting and generated a $2.6 billion operating loss.

The SEC effectively banned this practice for normal acquisitions in 2001 (this was a popular strategy in the dot-com boom) because it obscures the true costs of a merger4.

It retroactively restates financials as if SpaceX and xAI had always been one company.

This means investors cannot cleanly separate what the core space and connectivity businesses earn from what the AI segment burns.

The S-1 gives only three years of history, no segment balance sheets, and limited cash flow detail.

Public offerings typically disclose financials that help their case — which makes the absences here notable.

It appears a significant portion of the capital raised from the public in this IPO will essentially be used to pay off historic liabilities tied to the merger of xAi and X.

A Limitless Total Address Market

Per SpaceX’s S-1 Registration, it claims a total addressable market of $28.5 trillion.

For context, US GDP is between $24.2 to $31.8 trillion.

To claim, your TAM is the size of the entire US GDP elicits…a reaction.

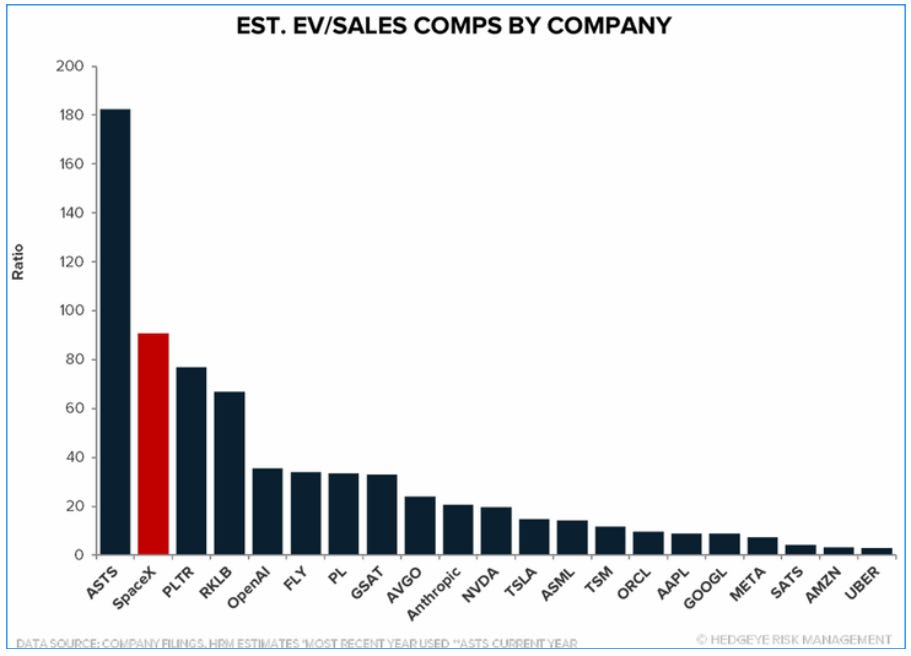

Price to Sales Above the Stratosphere

We should also consider its Price to Sales relative to recent history and longer history as well.

SpaceX is being priced close to 90x sales which is higher than every other AI company too.

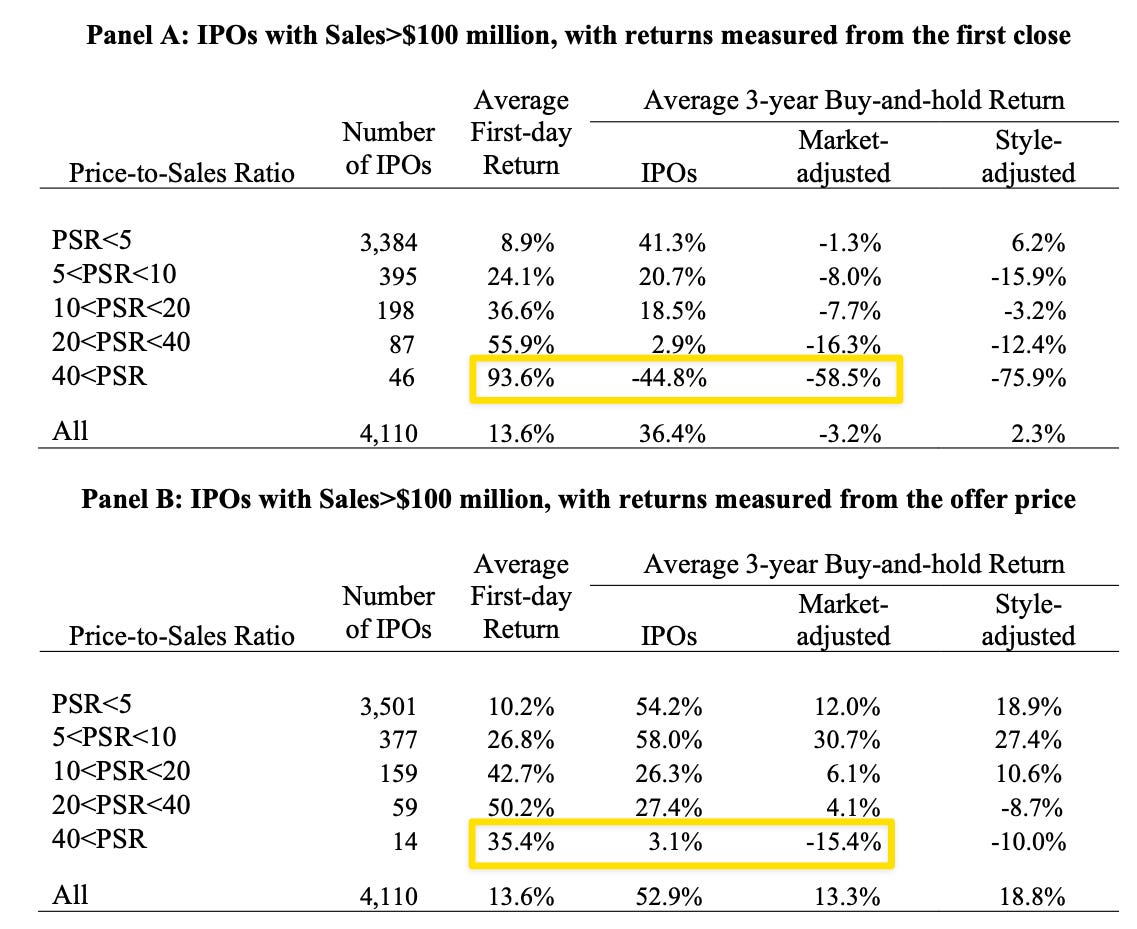

The following table is most illuminating as it highlights a -44.8% return as the average 3-Year Buy and Hold Return for someone who bought an IPO around 40x Sales (which is less than half of SpaceX at 90x) at the first day’s closing price.

This of course massively underperforms if you just had owned the market index (an underperformance of -58.5%).

Even if you were allocated to the initial IPO price and holding the aforementioned constant, a 3.1% return as the average 3-Year Buy and Hold Return is a massive relative underperformance to the broad market (an underperformance of -15.4%).

Actively Managing Passive Demand Buying

It seems SpaceX’s financial engineering should be added to the list of its impressive engineering capabilities.

Bending the Rules

As a reminder, an index like the Nasdaq 100 or the S&P 500 is a passive index i.e. any investment funds that track that index MUST buy the index and its components no matter what.

A Passive Index

If you give me cash then I will buy at any price,

If you ask for cash I will sell at any price.

Traditionally, major stock market indices like the NASDAQ 100 or the S&P 500 require a minimum “free float” of 5%-10% meaning at least 5%-10% of the company’s total shares must be publicly traded and available to everyday investors.

Additionally, when a company goes public, it must undergo a standard “seasoning period” (this can range from months to years) of public trading activity before it is allowed to be considered for inclusion into a major passive index.

It would awesome if one could financially engineer the trillions in wealth that track passive indexes to include your stock after IPO since they are by definition mindless buyers of whatever is in the index.

However, the rules would exclude SpaceX because Elon Musk and a tight circle of early private insiders intend to retain the vast majority of equity, SpaceX’s public listing may only float roughly 3.75% of its total value ($75 billion out of a $2 trillion valuation). Plus, it would be an IPO which means there wouldn’t be much of a seasoning period.

Or

You could have index providers begin changing rules to permit fast entry of IPOs into the indices that trillions in wealth must follow.

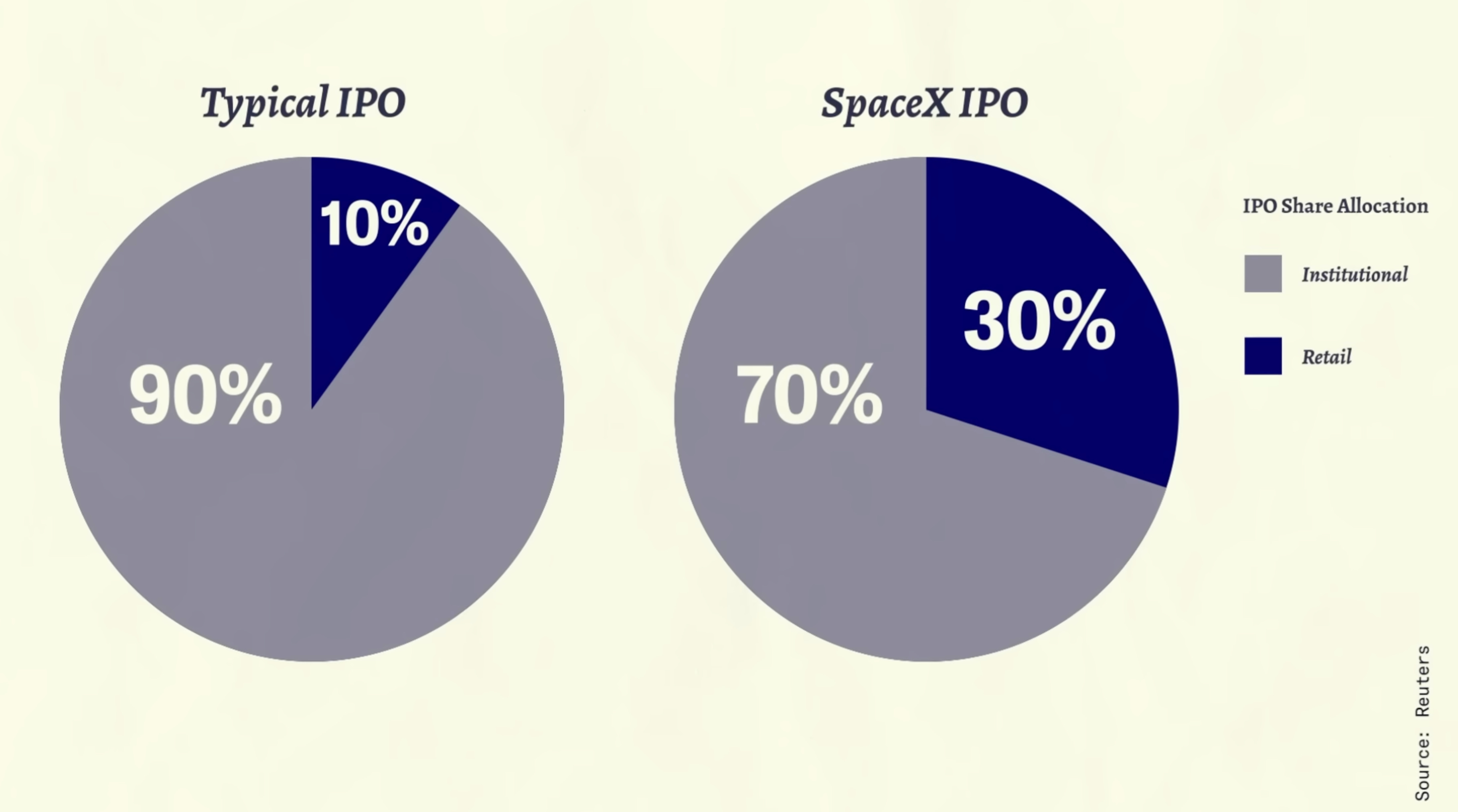

We must not forget that the typical IPO allocation has about 90% of shares allocated to institutional and 10% allocated to retail.

For the SpaceX IPO, it is setup to be 70% institutional and 30% retail.

So, we see the highest valuation in history for a company that isn’t profitable with uncharacteristically opaque financials while the index rules are conveniently changing so that a previously delayed tsunami of price agnostic buyers show up quickly while allocating more of these shares to retail…

And the supply of lockups eligible to be sold are the largest in 25 years to boot (Lockups are insider shares that become tradable once the lockup period from prior IPOs, SPAC mergers, M&A deals, and private funding rounds expire).

One thought springs to mind that has a familiar historical ring:

“Funding Secured”

~Elon Musk on August 7, 2018

The Verdict of History

SpaceX, for all its technical and engineering brilliance, appears to be a “perpetual capex machine,” forever needing capital (thus dumping more shares onto the public) to fund its interstellar ambitions.

Priced for absolute perfection, it leaves virtually no margin for error.

Therefore, when the bells ring and the financial anchors cheer the next great IPO, remember the historical mechanics of the game and the tragedy of Icarus.

The insiders are liquidating their stakes. The bankers are extracting their tithes. The institutional whales are securing their first-day profits.

By the time the shares reach the open market and fall into your portfolio, the ground floor is long gone.

You are not buying at the ground floor.

You are buying Icarus at the zenith of his journey to the sun.

Then

You will end up on the ground floor.

Finally, don’t conflate avoiding a company at its IPO as never owning the company.

Great companies have a much greater chance of providing great shareholder returns after the hype is over and its share price is far more grounded relative to the business’s fundamentals.

Disclaimer

This website is not an offer or solicitation in any jurisdiction in which the firm is not registered. Information presented is for educational purposes only. It should not be considered specific investment advice, does not take into consideration your specific situation, and does not intend to make an offer or solicitation for the sale or purchase of any securities or investment strategies. The services, securities and financial instruments described on this website may not be suitable for you, and not all strategies are appropriate at all times. Investments involve risk and are not guaranteed. Past performance is not necessarily a guide to future performance. Independent advice should be sought in all cases.

TYME Advisors is a U.S. Securities and Exchange Commission (SEC) Registered Investment Advisor . Registration does not imply a certain level of skill or training. Information about the firm including the Customer Relationship Summary is available on the SEC’s website at www.adviserinfo.sec.gov. Information about our privacy policy is located here.

Andrew Freeman, CFA: Communications Analyst at Hedgeye Risk Management

Jay Van Sciver, Industrials Analyst at Hedgeye Risk Management

Jay Van Sciver, Industrials Analyst at Hedgeye Risk Management

Jay Van Sciver, Industrials Analyst at Hedgeye Risk Management